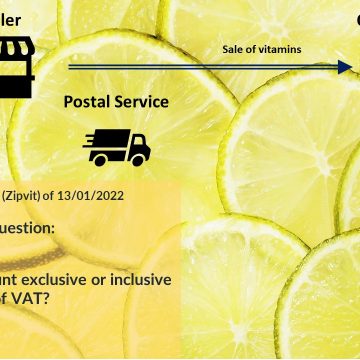

Is an invoice amount exclusive or inclusive of VAT?

on September 1, 2022

with No Comments

Invoice Is an invoice amount exclusive or inclusive of VAT? Version française Invoice with or without VAT? Discover the rules The importance of the contract for VAT purpose A business … Read More